Introduction

New charities attract

everyone’s attention - like new born babies, they are full of hope and promise

for the future. But what causes them to

lose their registered charity status?

Does deregistration really mean the end of the road, or do some flourish

without the oversight of a charity regulator?

And - perhaps most importantly - will the new deregistration tax result

in more resurrections than ever before? I

looked at the NZ charity data and discovered there really is life after death

in the charitable sector.

Summary

During the year ending 31

March 2015 (FY 3/15) there were 1,017 new charities registered in NZ – that’s

21 charities registered each week.

Australia registers an average of 49 charities a week, so on a

per-capita basis NZ charities are more prolific. But that picture changes when you realise the

NZ regulator deregistered 1,330 charities the same year – averaging 26

deregistrations a week. The result was a

net reduction of 313 charities on the

register for FY 3/15.

Deregistration means

there is no longer public transparency over the charitable assets or activities

of many of these organisations.

Incorporated societies are the exception – they must continue filing

financial reports with the Companies Office which are publicly available. Companies will also file annually with the

Companies Office and charitable trusts will lodge basic information with the

Companies Office, but financial information will no longer be publicly

available for most of these entities. Deregistered

charities must also start to file annual tax returns with Inland Revenue. Tax exemption will generally be lost unless

they are exempt under other provisions of the Income Tax Act (such as amateur

sports bodies); donee status (which enables donors to claim tax credits for

their donations) will not necessarily be lost – they may continue to qualify

under section

LD 3(2) of the Income Tax Act 2007 (ie if the organisation

is not carried on for the private pecuniary profit of an individual and its

funds are applied wholly or mainly to charitable, benevolent, philanthropic or

cultural purposes within NZ).

Information on the charities

register shows there are four reasons why charities are deregistered:

i. Failing to file a return:

The regulator will deregister

charities if they have two or more overdue Annual Returns. In FY 3/15, 61% (812) of all deregistrations were due to failure to file returns. Out of these, 575 had lodged at least one

return before the deregistration, so we know that the 575 controlled charitable

assets totalling $112.8m. The balance of

237 had never filed a return with the regulator so neither the public nor the

regulator know what charitable assets they controlled. The sector with the most deregistrations for

failing to file returns was “education / training / research” (19% of return

deregistrations) followed closely by “religious activities” (17%). If a charity is deregistered for not filing

returns, the average delay between their last public disclosure and

deregistration is 3 years and six months. Deregistered charities can

re-register, and many do. However the

regulator does not seem to require them all to file overdue returns as a

prerequisite to re-registration. Many others

continue operating post-deregistration without seeking to re-register.

ii.

Voluntary deregistrations: The number of voluntary

deregistration requests over time is fairly consistent, with 400-500 requests

lodged per annum over the last five years.

In FY 3/15, 38% (511) of all deregistrations were voluntary. Most of these charities have wound up or

merged with another charity. However,

some (194 in FY 3/15) tell the regulator they no longer need charitable status

and many of these organisations continue to operate without it. On the rare occasion a charity may

voluntarily deregister during, or as a result of, a regulator investigation (as

reported for The Glenn Family Foundation Charitable Trust). The sector with the most charity voluntarily

deregistrations in FY 3/15 was “education / training / research” (25% of

voluntary deregistrations were by charities in this sector).

iii.

Regulator

investigations uncover serious wrongdoing: The

regulator has deregistered seven charities for serious wrongdoing since

2008. The most common reason for serious

wrongdoing involved charities providing private benefits to their officers or related

parties. For example, when a charity pays

private expenses and makes undocumented or non-arms’-length loans. In three cases the regulator made orders under

section

31(4) to prevent an application for re-registration for a specified period

and it disqualified people from being an officer of another charity for a

specified period. Despite the charities

being deregistered, five of the seven appear to still exist, two still have

active IRD donee status, and officers of five of the seven deregistered

charities appear to be involved with other registered charities today. None of the deregistered charities

successfully applied to re-register as a charity.

iv.

Regulator

review determines that the organisation’s purposes are not charitable: Once a charity is registered, the regulator may decide to

initiate a review of its charitable purposes.

According to the charity register there have been 41 such reviews that

resulted in charities being deregistered.

A number of charities

were deregistered because they failed to meet the public benefit test. For example, they only provided benefits to a

closed group or membership, or they focused on sportspeople at an elite level.

Other

charities were deregistered because they had a charitable purpose and

a non-charitable purpose (and the latter was more than ancillary). For example, in addition to having a

charitable purpose some organisations had a purpose of providing recreation or

entertainment for private benefit (which is not charitable); they had a purpose

of promoting the private interests of a specific group (which is not

charitable); they had a purpose of promoting a point of view (which is not

charitable); and they had a purpose of promoting a change in public policy

(which is not charitable).

Based on the analysis that follows in

this paper, here some helpful tips for charities involved with deregistration:

i. If you want to voluntarily deregister: If

you want to voluntarily deregister because you are winding up, just letting the

charity regulator know may not be enough.

If you are a charitable trust, incorporated society or company, inform

the Companies Office at the same time.

If your charity is going to continue to exist after voluntary deregistration,

make sure you know what the tax implications are, especially how the new

deregistration tax affects your charity if you voluntarily deregister after 14

April 2014. You should also make sure

you know whether you will need to continue to report to the Companies Office

instead of the charities regulator. DIA

has a helpful guide for voluntary deregistrations on its website.

ii.

If you

don’t file your annual returns: If your charity is not meeting its return

filing obligations, expect to be deregistered once you have two returns

overdue. If you are deregistered and you

want to continue as a charity (and retain your tax exemptions) then reapply to

the charity regulator as soon as possible (definitely within 12 months of

deregistration or you will be subject to the new deregistration tax). It is worth

thinking about the pros and cons of re-registration – up to now, many deregistered

charities continue to operate after being deregistered and just switch their

reporting to meet the Companies Office requirements. Because losing registration doesn’t mean you

necessarily lose IRD donee status, donations to your organisation may still be

eligible for a tax credit. But a word of

caution – the past is not a good predictor of the future. Everything changed from 1 April 2015 with the

new deregistration tax, which may apply if you are deregistered by the

regulator after this date.

iii.

If you

want to avoid being deregistered for serious wrongdoing: Make sure you have good governance and good

record keeping. Simple.

iv.

If you

want to avoid being deregistered because you no longer qualify as a charity: Keep

an eye on the deregistration decisions being published by the regulator. If you have doubts about whether your charity

meets the public benefit test, or your charity has a non-charitable purpose

that starts to become a main purpose rather than an ancillary purpose, you may want

to get legal advice.

Finally, once your charity is deregistered,

make sure you update your charity’s website and documentation to make it clear it

is no longer a registered charity. If

you miss this step and you continue to refer to your deregistered organisation

as a registered charity, you are committing a “holding out” offence under section

37 of the Charities Act and could be liable on conviction to a fine of up

to $30,000.

In conclusion, there may be life after

death for deregistered charities. But

the charity regulator will still keep an eye on you in case you “hold out” as a

registered charity, and the taxman will be keen to see whether he can assess

you with a deregistration tax.

_________________________________________

The details

1. Deregistration trends:

reasons for deregistration

Graph A shows the trend

in the volume of deregistrations, and the reason for them, from 2009 to

2015. The NZ regulator began to regulate

in 2008 and all charities were required to apply for registration at that time,

resulting in about 20,000 applications (the register contains 27,197 charities

today). Using this one-off mass

registration approach is why there were few deregistrations until 2011 - when

some of the new charities failed to lodge their annual returns for the first

time. The NZ approach was quite

different to Australia’s, where 56,000 charity records were automatically transferred

from the Tax Office to the new regulator in 2012 and the charities did not have

to complete any application forms.

Consequently the Australian regulator’s task in its first two years was

to deregister those charities that no longer existed and obtain current details

from those that did exist.

Although the volume of voluntary

requests to deregister has remained relatively consistent from 2011, the volume

of deregistrations for failing to file an annual return has fluctuated

dramatically. This is largely driven by

the deregistration policy of the regulator.

For example, it initially made the decision to deregister charities with

just one overdue return, however from 2013/2014 it made the decision to only deregister

charities if they had two overdue returns.

This is why there were almost no overdue return deregistrations in the

year ending 31/3/14 (the catch-up year) and a higher volume in 31/3/15 to

address the growing number of delinquent charities.

Graph A

The volume of charities

deregistered as a result of compliance activities (for serious wrongdoing or

failing to respond to information requests) and as a result of reviewing

whether they qualify as a charity, has always been relatively low. Based on the register data, only seven

charities have been deregistered for serious wrongdoing since 2009 and 41 have

been deregistered because they did not qualify as a charity. The detail for these deregistrations is

explained later in this paper and the NZ

regulator publishes reasons for decisions on its website. However, the numbers on

the graph may not be exact because they rely on system codes to be

correct. In addition, many

organisations apply to register as charities and have their applications declined

– those decline decisions are not reflected in this graph.

2. Deregistration trends:

charities that never reported to the regulator

There have been 6,519

charity deregistrations between 2008 and October 2015. Out of the 6,519 deregistrations, only 4,254

charities had filed one or more returns with the regulator before

deregistration. That means approximately

2,265 charities did not publicly report on their charitable activities, despite

being registered charities (a small number of these may have filed reports but

the regulator agreed to withhold them from public view, as explained in its Restricting

Information policy).

Graph B shows the total number

of deregistrations since 2009 compared to the number of deregistrations where

at least one return had been filed. The

difference between the two lines represents the number of deregistered

charities that never filed a return whilst they were registered. The

deregistrations from 1 April 2015 to 31 October 2015 have been rounded to a 12

month period and included as a forecast figure for the year ended March 2016.

Graph B

3. Voluntary

deregistrations

The NZ regulator does not

have a specific deregistration form; charities simply send an email or letter

to the regulator requesting deregistration. Out of the 511 charities that requested

voluntarily deregistration between 1/4/14-31/3/15, 446 had lodged at least one

return. The top five sectors they

operated in (for those charities which filed a return) were education /

training / research 25% (110), health 13% (57), religious activities 12% (54),

social services 9% (41), and arts / culture / heritage 8% (34).

The voluntary

deregistration reasons, categorised by the regulator, were as follows:

i.

“No longer requires charitable status” was the category used by 38%

(194) of charities. 147 of these had filed

at least one return, the most recent showing total assets of $36m and total

equity of $31m. The top four sectors

these charities operated in were education/training/research (42), health (22),

arts/culture/heritage (13) and social services (13). Details of the top five

charities ranked by assets are shown below.

None of the five had IRD donee status.

It is likely that all five are still active even though they have

deregistered.

· Tuhoe Waikaremoana Maori Trust Board: Main sector – education/training/research; 31/3/14 assets - $10.6m.

The board appears to still be active

and making grants.

· The John Mitchell McLachlan Charitable Trust: Main sector – social services; 31/8/13 assets - $6.0m. The trust appears to still be active and

making grants.

· Stratford Charitable Trust: Main sector – emergency/disaster relief; 31/3/14 assets - $2.9m.

The trust is still registered as a

charitable trust with the Companies Office.

· Te Utuhina Manaakitanga Trust: Main sector – health; 30/6/13 assets - $2.1m. The trust is

still registered as a charitable trust with the Companies Office.

· The

Glenn Family Foundation Charitable Trust: Main sector – “other-evenly spread”; 31/3/14

assets - $2.4m (equity - $2.3m). This

trust voluntarily deregistered on 1/12/14.

It was reported to have done so after Internal Affairs abandoned an

investigation into alleged irregular payments for a thoroughbred racehorse made

by this charity (to Bloodstocks Ltd and Own Glenn’s account in Sydney), see “Glenn

charity probe dumped” 14/12/2014, Bevan Hurley, Herald on Sunday. Glenn is

reported to have said “I pulled out my Foundation from New Zealand” but it is unlikely

the trust subsequently distributed its net assets because the objectives in the

trust deed always had a focus on both NZ and India (and more recently the Pacific

Islands) and the trust is still active on the Companies Office charitable

trusts register. In its financial

statements for the year ended March 2014 the trust recorded donation income of

$3.9m from Corona Trust, incurred $742k on “Glenn Inquiry expenses” and made

donations of $1.2m to “Otara” and “Other”. Related party advances of $1.0m were made to

Go Bloodstock Ltd and a note explains these funds were repaid during the year

with interest at 5% per annum. The

Corona Trust is a family trust set up in the Caribbean tax haven of Nevis and

there have been media reports of a court battle for control of its $400m funds,

see “Daughter

helps dad fight for fortune”

25/5/14, Bevan Hurley, Herald on Sunday. This charity is also discussed in Blog 6: “NBR rich-listers

and charities”. When I wrote that blog in 2012 the charity had not filed any

returns but in its application to be a charity it had indicated that 50% of its

charitable activities would be carried out in Asia.

The 47 charities that deregistered under this category but had never

filed a public return included seven Tait Communications companies (they filed returns which were withheld and

recorded as “restricted” on the register) and 17 English Language Partners

charities (the did not file returns because they were part of a group).

ii.

“Wound up and distributed assets” was the category used by

31% (157) of charities. 149 of these

had filed at least one return, the most recent showing total assets of $87m and

total equity of $64m. The top four

sectors these charities operated in were education/training/research (35),

health (17), religious activities (17) and social services (17). Details of the

top five charities ranked by assets are shown below.

· Central North Island Kindergarten Association: Main sector – education/training/research; 31/3/12 assets -

$22.6m. Ceased as IRD donee 1/1/13 and

struck off the incorporated societies register managed by the Companies Office.

· St James Theatre Charitable Trust (Wellington): Main sector – arts/culture/heritage; 30/6/11

assets - $18.7m. Still an IRD

donee. Media suggests this trust was

integrated with the Wellington Convention Centre to form Positively Wellington

Venues in 2011. The trust has been struck off the charitable trusts register

managed by the Companies Office.

· Watch Tower Bible and Tract Society of NZ (charitable trust): Main sector – religious activities; 31/8/12

assets - $7.9m. Ceased as an IRD donee

but is still registered on the charitable trust register managed by the

Companies Office.

· Lakes Leisure Ltd: Main sector: sport / recreation; 30/6/11 assets - $4.7m.

Ceased as an IRD donee and struck off Companies Office register. This was a council controlled organisation.

· The Methodist Church of NZ (New Plymouth): Main sector – religious activities; 30/6/10

assets - $4.4m. Not recorded as an IRD donee organisation.

iii.

“No longer carrying on their operations” was the category used

by 24% (125) of charities. 116 of these had filed at least one return,

the most recent showing total assets of $96.0m and total equity of $75.9m. Details of the top five charities ranked by

assets are shown below.

· The North Shore Domain and North Harbour Stadium: Main sector – sport/recreation; 30/6/13 assets - $261.2m. This entity never had IRD donee status. Although the stadium is still operating, it

is difficult to ascertain the structure currently being used.

· Access Homehealth Ltd: Main sector – health; 30/6/13 assets - $16.9m. IRD donee

status ceased 30/11/14. The company is still registered with the Companies

Office, annual returns are being

filed (23/9/15) and it is trading – see its website. The

company was sold by Rural Women NZ (a

charity) to Green Cross Health Ltd, a for-profit company listed on the NZ stock

exchange, in November 2014. Green Cross

Health is a pharmacy retail group with approximately 300 pharmacies.

· The Unification Church of NZ Trust Board: Main sector – religious activities; 31/3/13 assets - $4.7m.

IRD donee status ceased 28/9/14. The purpose of this charity was to promote

adherence to the Divine Principle defined by the Reverend Sun Meung Moon – it

is a religion commonly referred to as the “Moonies” and is linked to the

still-registered Universal Peace Federation charity.

· Taranaki PHO Ltd: Main sector – health; 30/6/11 assets - $3.1m. Not recorded as

an IRD donee organisation.

· Bruce Mason Centre Board: Main sector – arts / culture / heritage; 30/6/13 assets -

$1.5m. Not recorded as an IRD donee

organisation. Stuck off the Charitable

trusts register 30/6/14.

iv.

“Merged with another charity” was the category used by 4% (19)

of charities. 18 of these had filed at

least one return, the most recent showing total assets of $9.9m and total

equity of $6.9m. Details of the top two

charities ranked by assets are shown below.

· Tipu Ora Charitable Trust: 30/6/13 assets - $4.5m.

This primary health organisation never had IRD donee status and was

struck off the Charitable trusts register on 10/10/14. Its website explains it combined with the Te

Utuhina Manaakitanga Trust to form Manaaki Ora Trust.

· South Taranaki Free Kindergarten Association Inc: 31/12/12 assets - $2.2m. IRD donee status ceased 25/2/15 and it was

struck off the Incorporated Societies register on 26/2/14. Its website explains that in March 2014 this

charity joined North Taranaki Free Kindergarten Association to create a single

organisation.

v.

No reason for deregistration was the category used by 2% (10) of

charities.

vi.

“No longer qualified as a registered charity” was the category

used by 1% (6) of charities. Five of these had filed at least one return,

the most recent showing total assets of $856k and total equity of $661k. Details of the six charities ranked by assets

are shown below.

· Estate of Gladys Valentine Howey: Main sector – care/protection of animals; 30/9/12 assets - $653k. This Estate did not have IRD donee status.

· The Eleazar Family Support Trust: Main sector – social services; 31/3/14 assets - $146k. IRD donee status ceased 27/2/15.

· Riparian Support Trust: Main sector – sport/recreation; 31/3/13 assets - $10k. IRD

donee status ceased 9/2/15.

· Tasman Trespasser Charitable Trust: Main sector – sport/recreation; 31/3/13 assets - $7k. IRD

donee status ceased 25/9/15.

· Help2save: Main sector – religious

activities; 31/3/13 assets - $0. This organisation did not have IRD donee

status.

· Bereaved Whanau Suicide Support trust. IRD donee status ceased 17/2/15.

4. Deregistered by

regulator – failure to file returns

Unlike charities that

voluntarily deregister, charities that are deregistered by the regulator for

not filing returns are seriously non-compliant.

They did not engage with the regulator and they did not disclose their recent

financial information to the regulator or the public, despite receiving tax and

other benefits.

The NZ regulator has the

authority to deregister a charity that has “significantly and persistently”

failed to comply with the Charities Act (refer to section

32(1)(b) of the Charities Act 2005). Its current policy is to deregister charities

if they have two or more overdue Annual Returns, because that triggers the “significantly

and persistently failed to comply” criteria.

More information is contained in the February 2015 Charities Update newsletter. There is nothing

to stop a deregistered charity from submitting a new application and there is

no charge for re-registering. Although

you would expect all overdue returns must be filed first, analysis in Table 1

below indicates this may not always be the case. The Australian regulator has a similar policy of

deregistering charities that have not filed for two years, however they must

file overdue returns before re-registration is considered.

Out of the 812 charities

that were deregistered between 1/4/14-31/3/15 for failing to file two or more

returns, 575 had lodged at least one return and 237 had never filed a return

with the regulator. The top five sectors

they operated in were education / training / research 19% (158), religious

activities 17% (134), arts / culture / heritage 11% (88), social services 7% (58)

and sport / recreation 6% (52). Based on

the most recent return filed by the 575 charities that had filed a return, these charities received a total of $7.0m

donations, $57.4m gross income, controlled $112.8m assets and had $57.5m

equity.

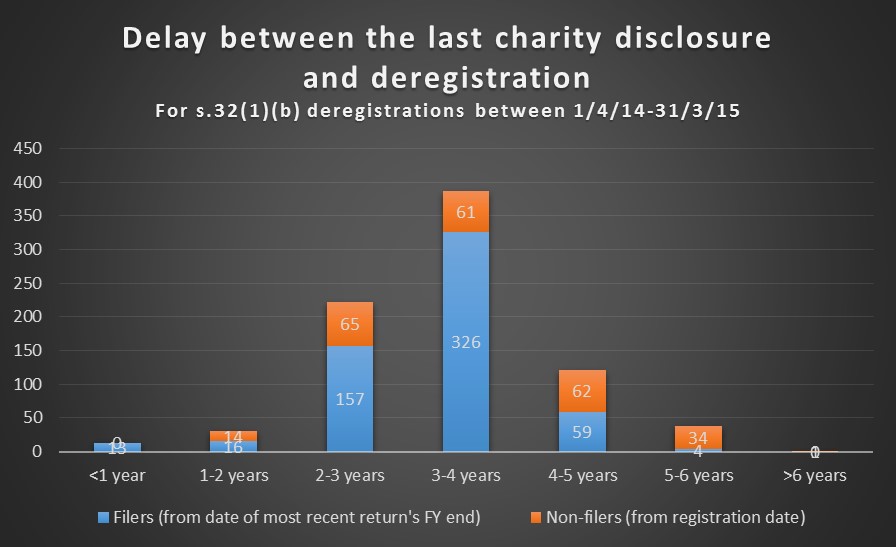

Graph C shows the delay that occurs between the time of

the last charity disclosure and the deregistration date (for the 812 charities

deregistered between 1/4/14 and 31/3/15).

For example, if a charity filed its last return for the year ending

31/3/11 and was deregistered in January 2015, it will have been 3 years and 10

months from the date of their most recently reported financial information to

deregistration. A charity will fall in

the same category if it was registered on 31/3/11, never filed a return and was

deregistered in January 2015. This gap

is important, because it highlights the period when an organisation can

continue to benefit from tax exemption and credibility as a registered charity,

despite not informing the public or the regulator about its charitable

activities. If this gap cannot be

reduced by the regulator, at the very least it would be useful to the public if

the charities’ filing non-compliance is highlighted through a warning on the

register prior to deregistration (as is done in Australia, using a statement in

red to indicate how long returns are overdue).

[Charities with returns filed within one year of the

deregistration date are generally anomalies, for example they filed returns

after being deregistered, such as the Rotary Club of Alfriston Incorporated

Charitable Trust, which was deregistered on 30/7/14 but lodged its 2014 return on

25/8/14.]

Graph C

Table 1 shows 10

charities with the largest value of donation income in their most recently

filed return before deregistration. There

are two notable points from this list:

·

Three charities subsequently

re-registered but they were not required by the charity regulator to lodge the

outstanding returns which caused their deregistration.

·

Inland Revenue did not

remove donee status for four deregistered charities, despite their significant

and persistent breach of the Charities Act (the worst case had not filed any

returns since March 2011).

Table 1: Charities with

largest donation income that were deregistered 1/4/14-31/3/15 for not filing

returns

Charity legal name

|

Last return

|

Dereg Date

|

Donation Inc

|

Total Assets

|

Re-registered

|

IRD donee status

|

|

1

|

Free Wesleyan Church of Tonga in New Zealand Trust Board

|

31/12/13

|

11/2/15

|

$1,015,385

|

$16,958,323

|

Yes-28/5/15 (but 12/14 return not filed)

|

Yes

|

2

|

Blenheim Baptist Church

|

31/7/11

|

8/1/15

|

$332,072

|

$1,971,440

|

Yes-5/1/15 (but 7/12, 7/13, 7/14 returns not filed)

|

Yes

|

3

|

Mizpah Church Charitable Trust Board

|

31/3/11

|

27/1/15

|

$306,566

|

$1,768,584

|

No

|

No – ceased 14/4/15

|

4

|

Hillary House Leadership Centre Trust

|

31/12/11

|

11/2/15

|

$297,924

|

$350,750

|

Yes-13/4/15 (but 12/12, 12/13, 12/14 returns not filed)

|

Yes

|

5

|

Waimea Plains Railway Trust

|

31/3/14

|

3/2/15

|

$275,652

|

341,454

|

Yes-12/2/15 (3/15 return IS filed)

|

Yes

|

6

|

Papakura Samoan Assembly of God

|

31/3/12

|

9/12/14

|

$190,790

|

$1,296,738

|

No

|

No

|

7

|

Missionaries of Faith Trust

|

31/12/11

|

10/2/15

|

$184,601

|

$923,427

|

No

|

Yes

|

8

|

Ahmadiyya Anjuman Isha’at-I-Islam Lahore (New Zealand) Trust

|

31/3/12

|

17/2/15

|

$179,350

|

$177,498

|

No

|

Yes

|

9

|

METHODIST CHURCH SAMOA (NEW ZEALAND HENDERSON PARISH)

|

31/3/12

|

17/2/15

|

$178,500

|

$2,667,032

|

No

|

Yes

|

10

|

The Waitaki Valley Medical Trust

|

31/3/11

|

2/2/15

|

$164,100

|

$298,035

|

No

|

Yes

|

Table 2 shows 10

charities with the longest duration between registration and being deregistered

and who never filed a return with the regulator. There are three notable points from this

list:

·

The first issue

highlighted in Table 1 applies here, where one charity re-registered but was

not required by the charity regulator to lodge the (five) overdue returns which

caused its deregistration.

·

The second issue

highlighted in Table 1 also applies here, where Inland Revenue did not remove

donee status for three deregistered charities, despite their significant and

persistent breach of the Charities Act.

·

Better co-ordination

between MBIE (Companies Office), IRD and DIA Charities is likely to help reduce

red tape for charities and align information so that registers are more accurate. For example, one charity was stuck off by the

Companies Office as an incorporated society in 2010 and IRD removed its donee

status in 2010, but the charity regulator did not remove it until 2014; another

was struck off by the Companies Office as a charitable trust in 2011 but was

not deregistered by the charity regulator until 2014 and did not have its IRD

donee status removed until 2015. One registered

charity continued filing returns on the incorporated society register and never

filed with the charity regulator for 5 years.

Table 2: Non-filing

charities with the longest duration between registration and deregistration

(that were deregistered between 1/4/14-31/3/15)

Charity legal name

|

Main sector

|

Last known Chairperson / Trustees

|

Reg. Date

|

Dereg. Date

|

Re-registered

|

Still active?

|

IRD donee status

|

|

1

|

Community

Events Trust NZ

|

Arts / culture / heritage

|

Sharon Lingham

|

18/03/2008

|

30/07/2014

|

No

|

No – S Lingam passed away in 2010

|

No

|

2

|

Asia

Pacific Arts and Cultural Trust

|

Arts / culture / heritage

|

Thakur Ranjit Singh, Ami Chand,

Binesh Kumar Sumer

|

3/02/2009

|

21/01/2015

|

No

|

Likely – still registered as a charitable trust

|

Yes

|

3

|

Mamaku

Community Youth And Family Incorporated

|

Community development

|

Aneta McMeeking

|

22/01/2009

|

18/12/2014

|

No

|

No – struck off as Inc Society 27/9/10

|

No-ceased 27/10/10

|

4

|

Hawkes Bay

Song and Opera Workshop Incorporated

|

Arts / culture / heritage

|

Anita Louise Davies

|

25/01/2009

|

16/12/2014

|

No

|

Highly likely – still registered as a charitable trust;

presented awards in 2013

|

Yes

|

5

|

Blackball

Volunteer Fire Brigade

|

Emergency / disaster relief

|

Mark Boere

|

20/04/2009

|

5/12/2014

|

Yes – 18/5/15 -5 o’due returns not filed

|

Yes

|

No

|

6

|

Tokomairiro

Youth Advantage Trust

|

Other - PROMOTION OF WELL-BEING

OF YOUTH

|

Jill Christine Mcintosh, Andrew

Robert McIntosh, 7 others

|

6/01/2009

|

30/07/2014

|

No

|

No – struck off as a charitable trust 1/8/11

|

No – ceased 27/2/15

|

7

|

Kumeroa-Hopelands

Playgroup

|

Education / training / research

|

Carolanne Sixtus

|

19/01/2009

|

30/07/2014

|

No

|

Yes – referred to in 2015 school newsletter

|

Yes

|

8

|

Rotary

Club of Pahiatua Charitable Trust

|

Education / training / research

|

Alan Holdaway, Robin Whiteman,

3 others

|

1/02/2009

|

30/07/2014

|

No

|

Likely. Settled by the Rotary Club of Pahiatua Inc, but

not under the Charitable Trusts Act 1957 so no other reporting.

|

No-ceased 9/7/15

|

9

|

Lake

Brunner Emergency Services Society Incorporated

|

Emergency / disaster relief

(linked to Moana Vol Fire Brigade)

|

Anthony David Larkin

|

16/02/2009

|

30/07/2014

|

No

|

Likley. Still a

registered incorporated society.

|

No-ceased 25/2/15

|

10

|

Southland

Mangaia Club Incorporated

|

Arts / culture / heritage

|

Alexander Marie

|

16/07/2009

|

16/12/2014

|

No

|

Highly likely. Still a registered incorporated society,

filed returns to 2012.

|

No-ceased 10/4/14

|

5. Deregistered by

regulator – investigation findings of serious wrongdoing

The charities register

shows there have been seven charities deregistered for serious wrongdoing under

s.32(1)(e) of the Charities Act from the time the Charities Commission

commenced to October 2015. The details

of each charity deregistered, the reasons for deregistration and the current

state of the deregistered charity, are shown in Table 3. Here are my observations:

· Four of the deregistered charities were charitable trusts, which

are all still registered with the Companies Office today. Two were incorporated societies, of which one

has been liquidated and the other is still registered with the Companies Office. The remaining charity appears to have been unincorporated

and it is unlikely to exist but this is not certain.

· Officers of five of the seven deregistered charities are still

involved with other registered charities today.

· Despite being deregistered for serious wrongdoing, two still

have active IRD donee status, one donee status was removed 10 months after

deregistration and one was removed 11 months after deregistration. There is only one case when donee status was

removed on the same day as deregistration.

· In its early years, the charity regulator published its formal

decision analysis papers on the charities

register decisions page. However,

out of the four serious wrongdoing deregistrations that occurred in 2014 and

2015, only one had its decision analysis published. For the remaining three

deregistrations, the media reported the reasons for two deregistrations and one

deregistration was not explained or mentioned by the regulator or the media.

· In its early years, if the charity regulator identified serious wrongdoing

it would deregister the charity and make orders under section

31(4) to prevent an application for re-registration for a specified period

and disqualifying an officer of the entity from being an officer of a

charitable entity for a specified period up to five years. However the regulator has not made any orders

under section 31(4) for the four most recent deregistrations in 2014 and

2015.

Table 3

Charity legal name

|

Dereg Date

|

Media / regulator

explanation

|

Current state of deregistered

charity

|

|

1

|

Location:

Henderson, Auckland

Main

sector: Education

Chairperson:

Donald Too

|

27/07/2015

|

· The

register states this charity was removed for serious wrongdoing under section

32(1)(e) of the Charities Act 2005.

· Tens of thousands of dollars were allegedly gambled away

at casinos or spent on a motel in Samoa and the manager, Siaifoi Lisa Palmer,

transferred money to her personal account. She claimed this was the repayment

of a loan but did not have records to verify this claim. Palmer had a prior dishonesty conviction and

was disqualified from being a charity officer. See: “Govt

investigates West Akld charity” 7/11/15 Radio NZ.

|

· The organisation still has IRD donee status and is still

a registered incorporated society with the Companies Office.

· Chairperson Donald Too is currently an officer of

registered charity Transformed-Youth

Ministry.

|

2

|

Location:

Hamilton

Main

sector: Education

Trustee:

Southern Cross Trustee Ltd

|

27/05/2015

|

· The

register states this charity was removed under section 32(1)(a) and section

32(1)(e) of the Charities Act 2005.

· The published

regulator decision states a person associated with the trust (Robert

Wickham, the sole shareholder of the trustee company and a property developer)

engaged in serious wrongdoing and the trust no longer qualifies for

registration as it has an independent purpose to advance the private

pecuniary profit of the trustees through conferring private benefits on

related parties. The private benefits

involve 45 loans exceeding $25m to investment projects in which Wickham had

an interest, which either ended in losses or returns at below market rates.

|

· The organisation never had IRD donee status, however it

is still a registered charitable trust with the Companies Office.

· Southern Cross Trustee Ltd is still a registered company

with Robert Bryan Lathan Wickham the sole shareholder and director. It filed its annual return with the

Companies Office on 16/10/15.

|

3

|

Location:

Carterton, Wairarapa

Main

sector: Community development

Chairperson:

Henry Phillip Jacobs

|

30/06/2015

|

· The

register states this charity was removed for Serious Wrongdoing, section

32(1)(e) Charities Act 2005

· I could

not find any further detail on the regulator’s website or in the media about

this deregistration.

|

· The organisation still has IRD donee status.

· This appears to be a Baptist charity linked to Youth Aflame, an

international organisation. However

the nature of the legal entity is unclear – it is not listed as a charitable

trust or incorporated society so it is possible that it no longer exists.

· Two charity officers, Henry Phillip Jacobs and Carol Joy

Jacobs are still / have been officers for registered charity Koinonia

Christian Fellowship in Masterton.

|

4

|

Location:

Wellington

Main

sector: Social services

Chairperson:

Marcelle Philpott

|

28/02/2014

|

· The

register states this charity was removed under section 32(1)(a) and section

32(1)(e) of the Charities Act 2005.

· Media

reported the bulk of donations appear to have disappeared – spent on junk

food, booze and electronics by founder Michael Hawkins. Only 4% of $770,000

donations went to the needy. See “Wellington

foodbank probed for fraud” 28/2/14, Stuff, Ben Heather.

|

· IRD donee status was ceased on 16/12/14.

· The incorporated society is ‘in liquidation’ with the

Companies Office from 9/12/13.

· It was reported another company was subsequently set up

called Wellington Food Angels Ltd but this went into liquidation on 19/12/13.

· Chairperson Marcelle Philpott is still the officer of

registered charity Capital

Performing Arts Incorporated.

|

5

|

Location:

Hamilton

Main

sector: Social services

Initial

trustees: Aaron Wineera Elkington and Phyllis Millward Elkington

|

25/05/2011

|

· The

register states this charity was removed pursuant to section 32(1)(e) of the

Charities Act 2005, based upon the Commission’s finding of serious wrongdoing

committed by the entity, with effect from 25 May 2011. Orders were made under

section 31(4) to disqualify officers Aaron Elkington and Phyllis Elkington

until 25 May 2014, and disqualify Jonathan Clary until 25 November 2011, and

prevent re-registration of this entity before 25 May 2014.

· The published

regulator decision states funds for the trust were mixed with personal

funds of the trustees and spent on purchases at restaurants, cinemas, a

television, etc.

|

· IRD donee status was ceased on 9/4/12 however it is

still a registered charitable trust with the Companies Office.

· None of the three disqualified individuals are currently

involved with registered charities.

|

6

|

Location:

Christchurch

Main

sector: People with disabilities

Initial

trustees: David Charles Williamson and Anne Crawford Wadsworth

|

9/07/2010

|

· The

register states this charity was removed by the Charities Commission under

section 32(1) of the Charities Act 2005 with effect from 9 July 2010. Orders

were made under section 31(4) to disqualify the officer David Williamson

until 9 July 2013 and prevent re-registration of this entity before 9 July

2013.

· The published

regulator decision states the trust deed required a minimum of two

trustees but only had one for some time and did not notify the regulator of

changes; the trust made payments for private expenses and a $4,000 loan to

its trustee in contravention of its deed; there was no documentation for the

$4,000 loan; the trust could not provide documentation to support the bank

balance in its financial statements; the trust could not verify who its

$2,000 grant payment went to (inmates).

|

· The organisation has not re-registered as a charity.

· The organisation never had IRD donee status, however it

is still a registered charitable trust with the Companies Office.

· David Williamson is an officer of the currently

registered Canterbury

Ice Hockey Association Inc.

|

7

|

Location:

Christchurch

Main

sector: Fundraising

Initial

trustees: David Charles Williamson and David Francis Williamson

|

9/07/2010

|

· The

register states this charity was removed from the Charities Register by the

Charities Commission under section 32(1) of the Charities Act 2005 with

effect from 9 July 2010. Orders were made under section 31(4) to disqualify

the officer David Williamson until 9 July 2013 and prevent re-registration of

this entity before 9 July 2013.

· The published

regulator decision states there were discrepancies in the accounts; the trustee

said he made a $4,000 loan to the charity and reimbursed himself but there

was no documentation of the loan; the trust paid for private electricity and

telecommunications costs; the trust claimed in its fundraising to be raising

money for child cancer organisations, Lions and Rotary but in fact it

provided cash to young offenders and families in need; the trust deed

required a minimum of two trustees but only had one for some time and did not

notify the regulator of changes.

|

· The organisation has not re-registered

· IRD donee status was ceased on 9/7/10 however it is

still a registered charitable trust with the Companies Office.

· David Williamson is an officer of the currently

registered Canterbury

Ice Hockey Association Inc.

|

6. Deregistered by

regulator – review of charitable purposes

The regulator will always

review an organisation’s purposes before approving its application to be a

registered charity. However, once a

charity is registered, the regulator may decide to initiate another review of

its charitable purposes. It may do this,

for example, if the charity lodges amended governing documents, or if the

regulator receives a concern from an individual or agency. According to the charity register there have

been 41 reviews that resulted in charities being deregistered. The deregistration occurs under section

32(1)(a) on the grounds that the organisation no longer qualifies as a

charity.

The details of the most

recent 20 deregistration decisions are shown in Table 4. Here are my observations:

· A number of charities were

deregistered because they failed to meet the public benefit test. For example, they only provided benefits to a

closed group or membership, or they focused on sportspeople at an elite level

· A number of charities were

deregistered because they had a charitable purpose and a non-charitable

purpose (and the latter was more than ancillary). For example, in addition to having a

charitable purpose some organisations had a purpose of providing recreation or

entertainment for private benefit (which is not charitable); they had a purpose

of promoting the private interests of a specific group (which is not

charitable); they had a purpose of promoting a point of view (which is not

charitable); and they had a purpose of promoting a change in public policy

(which is not charitable).

Table 4

Charity legal name

|

Dereg Date

|

Reason for deregistration (published on the regulator “view

the decisions” site)

|

|

1

|

New

Zealand Global Women

|

9/10/2015

|

The

regulator determined that the Trust provides private benefits to a closed

group, so does not provide significant public benefit.

|

2

|

New

Zealand Rowing Association Incorporated

|

9/10/2015

|

The

regulator determined that the purposes of the organisation are to promote

rowing itself and to promote success in rowing at an elite level. These purposes are not charitable.

|

3

|

The Cellar

Club Incorporated

|

27/01/2015

|

The

Society promoted understanding and appreciation of wine through wine tastings

and vineyard visits. The regulator

determined that the Society is maintained for recreational purposes for the

private benefit of members and its non-charitable purposes are not ancillary

to charitable purposes.

|

4

|

Swimming

New Zealand Incorporated

|

30/10/2014

|

The

regulator determined that the purposes are to promote success in competitive

swimming at an elite level. Developing

and supporting elite athletes and promoting a particular sport is not

charitable.

|

5

|

New

Zealand Affordable Art Trust

|

27/03/2014

|

The Trust

promotes NZ artists. The regulator

determined that the Trust’s primary purpose is to promote the private

interests of artists, which is more than incidental to any charitable

purposes.

|

6

|

Awanui-Waipapakauri

Pony Club

|

19/02/2014

|

Decision

not published

|

7

|

Hawera

Cinema 2 Trust

|

30/10/2013

|

The Trust

submitted that it advances education, relieves poverty, and is beneficial to

the community by enhancing the district and sponsoring charitable

organisations. The regulator determined that the Trust’s dominant purpose is

to provide a movie cinema for entertainment. Entertainment/recreation is

outside the scope of charity unless it advances another charitable purpose.

|

8

|

Kind

Mothers Project

|

29/08/2013

|

Decision not

published

|

9

|

Move 2 New

Zealand Trust (Christchurch)

|

4/07/2013

|

Decision

not published

|

10

|

The Opera

House Trust

|

15/04/2013

|

Decision

not published

|

11

|

Loyal

Orange Institution of New Zealand Incorporated

|

30/11/2012

|

Decision

not published

|

12

|

Association

of Local Government Engineering New Zealand Incorporated

|

19/11/2012

|

The

Society’s purposes include upholding the status of engineering and management

of public assets in NZ. The regulator

determined that a main purpose of the Society is to promote the profession

for the benefit of members of that profession, which is not a charitable

purpose but a private benefit to members of the profession.

|

13

|

QLCHT

Developments Limited

|

5/11/2012

|

The

regulator determined that the company’s purpose is to further the purposes of

the Queenstown Lakes Community Housing Trust, which has been found not to be

charitable. It follows that this

company cannot be considered charitable.

|

14

|

The

Immunisation Awareness Society Incorporated

|

19/10/2012

|

While the

stated purposes of the Society are to advance education, the regulator

determined that its main purpose is to promote a point of view (that

vaccination is ineffective and dangerous).

The promotion of a point of view lies outside the legal definition of

a charitable purpose to advance education.

The regulator also determined that it is a purpose of the Society to

seek a change in public policy in regard to vaccination. That non charitable political purpose is

not ancillary to any valid charitable purpose.

|

15

|

Wakatere

Sailing Development Trust

|

24/11/2011

|

The

purposes of the trust include advancing the education of persons involved in

yachting at all levels. In its first three years it provided financial

assistance to 17 sailors. The

regulator determined that the main purpose was to provide assistance to elite

sailors and therefore there was not sufficient public benefit.

|

16

|

The Food

and Agribusiness Market Experience Alumni Trust

|

27/09/2011

|

The

purpose of the trust include advancing education, in particular to fund

research related to the agribusiness sector.

The regulator determined that identifying speakers and topics for

conferences for 60 alumni members, and arranging networking events, did not

amount to objective research available to the public and did not advance

education.

|

17

|

Rotary

International District 9980 Incorporated

|

27/09/2011

|

This

Society is responsible for overseeing, coordinating and facilitating

activities of 30 Rotary Clubs south of the Rangitata River. The regulator had considered many

applications for Rotary clubs and determined they did not have charitable

purposes. However it did register

trusts set up by Rotary clubs that are solely focused on carrying out service

activities.

|

18

|

Queenstown

Lakes Community Housing Trust

|

15/07/2011

|

High Court

judgement.

|

19

|

Mokorina

Whanau Trust

|

25/05/2011

|

The

trustees of this Trust were the parents and their three daughters. The only people to receive benefits were

the trustees (assistance to pursue university studies). The trust would only assist the trustees

and their descendants. The regulator

determined that the benefits are only available to a small number of people

and therefore does not provide benefits for the general public.

|

20

|

The

Business In The Community Charitable Trust

|

14/04/2011

|

The

purposes of this company included promoting businesses and new business

opportunities. Its charitable purposes

were advancement of education and other matters beneficial to the community.

The regulator determined its primary purpose is to provide business mentoring

services to the business community and in particular ‘for-profit’ businesses,

which does not advance education or learning.

|

The earlier 21

deregistrations for failing to qualify as a charity were for the following

organisations: Business in the community Ltd; Education Christchurch; Harbour

Lights Hall Society Trust; Fitness for Kids Trust; Film Central North Island

Trust; The William Kennedy Memorial Trust; Film Auckland Incorporated;

Kahungatanga New Zealand; Film New Zealand Trust; ICE Funds Limited; The

Icehouse Limited; National Council of Women of New Zealand Incorporated;

Octagon Market Trust; First Home Ownership Trust; New Zealand Computer Society

Incorporated; Enterprise Central Network Incorporated; The Joanne Wilson

Medical Trust Board; The Lyttelton Information and Resource Centre Trust;

Matakana Information Centre Incorporated; Grey Lynn Farmers' Market

Incorporated; Purple Patch (Tauranga) Incorporated.

7. The new deregistration

tax

From April 2014 new tax

laws for deregistered charities began to apply, which will soon have a big

impact on many deregistered charities across the country. As a result, NZ charities will need to

distribute their “accumulated income and assets” within 12 months of being

deregistered, or alternatively they will need to re-register as a charity

within 12 months of being deregistered, otherwise they will be subject to the income

tax. There are exceptions, for example

if they are entitled to another tax exemption, such as the amateur sports body

exemption, they will not be subject to the income tax.

Australia does not have a

similar law, but Canada does. The

introduction of the new law in NZ can be linked to the introduction of new reporting

standards for registered charities, which apply for all financial years

beginning on or after 1 April 2015. So,

for example, if a number of charities decided to voluntarily deregister in

order to avoid complying with the new reporting standards, they would be caught

by the new tax laws.

As explained on Inland

Revenue’s “Deregistration of charities” website, the tax change is being

introduced over time. Any charity that voluntarily

deregisters from 14 April 2014 and has not distributed its accumulated income and assets within

12 months will be subject to the tax.

However if a charity is deregistered by the regulator, for example

because it has failed to lodge two returns, is found to be involved with

serious wrongdoing, or is found to no longer qualify as a charity, then the new

law applies from 1 April 2015. So, for example, if a charity is deregistered

by the regulator in April 2015, then the charity must either re-register or distribute

its accumulated income and assets before April 2016 in order to avoid the tax.

The tax liability

calculation is not straight forward. To

establish when the 12-month period begins and ends, you must establish the date

of “final deregistration decision”, which is generally the later of the date

the charity is removed from the Charities Register or the date that all appeals

or court proceedings are finalised or exhausted. However, the date may be earlier if the

charity stopped complying with its rules held on the charity register or never

complied with its rules held on the charity register. In those cases the entity

will either be subject to income tax on the date it stopped complying with its

rules, or the date it was registered.

Then, to calculate the

net income and asset balance at the end of the 12-month period, you must take

the organisation’s assets less liabilities at the end of that 12-month period

and deduct:

· The value of any assets received from the Crown to settle a

Treaty of Waitangi claim

· The value of any assets received from the Crown under the Maori

Fisheries Act 2004

· Assets, other than money, gifted or left to the entity when it

met the requirements for exempt income.

Some charities that

voluntarily deregistered from 14 April 2014 will already be subject to this

tax. For example, between 14 April 2014

to 8 November 2014, a total of 250 charities voluntarily deregistered. If any of these 250 charities have not

distributed their “accumulated income and assets” by now, which is at least 12

months after their deregistration, they will be subject to the new tax and must

file a tax return for the year ending 31 March 2016 to include their

accumulated income and assets as taxable income. The charities register shows that out of the

250, 227 had filed a past return disclosing total net assets of $119.4m, so the

potential amount of tax liability could be significant. Even this figure does not include net assets

of the seven Tait Communication companies which were withheld from the public

register. Their net assets would,

presumably, had been very significant and subject to tax if they had not been

distributed before 18/9/15.

In the eight weeks

between now and 31 December 2015, the voluntarily deregistered charities with

the biggest potential exposure to the deregistration tax, if they do not

reregister or distribute their accumulated income and assets immediately, are:

i.

The Glenn Family

Foundation Charitable Trust. This charity voluntarily

deregistered on 1/12/14 so if it does not re-register or distribute accumulated

income and assets by 30/11/15 it is likely to be subject to the deregistration

tax. In its final return for the period

ending 31/3/14 its net assets were $2,335,250 so the potential tax liability at

the trust tax rate of 33%, assuming net assets did not change and no

adjustments are required, is $770,633.

ii.

Access Homehealth Ltd. This charity voluntarily deregistered on 1/12/14 so if it

does not re-register or distribute accumulated income and assets by 30/11/15 it

is likely to be subject to the deregistration tax. In its final return for the period ending

30/6/13 its net assets were $5,922,946 so the potential tax liability at the

company tax rate of 28%, assuming net assets did not change and no adjustments

are required, is $1,658,425.

Charities most affected

by the tax may be those which were deregistered for failing to file their

returns. They make up the largest group

of deregistrations and, unlike charities that voluntarily deregister, have not

usually turned their minds to their reporting obligations or the tax consequences

of being deregistered. Here is a list of

the first charities with potentially the biggest tax liabilities that will be

caught in this category, ie the charities that were deregistered between 1

April 2015 - 30 June 2015 for not filing their returns, and which will be

subject to the tax if they do not re-register or distribute accumulated income

and assets within 12 months (before 31 March 2016 – 29 June 2016).

i.

The Te Rau Aroha

Trust. This

charity was deregistered for failing to file a return on 21/4/15 so if it does

not re-register or distribute accumulated income and assets by 20/4/16 it is

likely to be subject to the deregistration tax.

In its most recently filed return for the period ending 31/3/11 its net

assets were $22,220,158 so the potential tax liability at the trust tax rate of

33%, assuming net assets did not change and no adjustments are required, is

$7,332,652.

ii.

Foundation For The

National Hockey Stadium. This charity was deregistered for

failing to file a return on 3/6/15 so if it does not re-register or distribute

accumulated income and assets by 2/6/16 it is likely to be subject to the

deregistration tax. In its most recently

filed return for the period ending 30/9/12 its net assets were $2,805,902 so

the potential tax liability at the trust tax rate of 33%, assuming net assets

did not change and no adjustments are required, is $925,948.

iii.

Nukutukulea Aoga Niue

Incorporated. This

charity was deregistered for failing to file a return on 17/6/15 so if it does

not re-register or distribute accumulated income and assets by 16/6/16 it is

likely to be subject to the deregistration tax.

In its most recently filed return for the period ending 30/6/12 its net

assets were $930,331 so the potential tax liability at the company tax rate of 28%,

assuming net assets did not change and no adjustments are required, is $260,493.

Looking across the Tasman

There

are several fundamental differences between Australia and NZ in respect of

deregistering a charity:

·

In

order to deregister a charity the NZ regulator may find that there has been a

significant or persistent failure by the entity to meet its obligations or it

may find the entity or a person connected with it has engaged in serious

wrongdoing. However, the Australian

legislation is more comprehensive. Across

the Tasman, the regulator must take into account the following matters

before it deregisters a charity:

(a) the nature,

significance and persistence of any contravention of the ACNC Act or non‑compliance

with a governance standard or external conduct standard (or any such

contravention or non‑compliance that is more likely than not) by the registered

entity;

(b) what action the

Commissioner, the registered entity, or any of the responsible entities of the

registered entity, could take or have taken:

(i) to address any such contravention or

non‑compliance (or prevent any such contravention or non‑compliance that is

more likely than not); or

(ii)

to prevent any similar contravention or non‑compliance;

(c) the desirability of

ensuring that contributions to the registered entity are applied consistently

with the not‑for‑profit nature, and the purpose, of the registered entity;

(d) the objects of any

Commonwealth laws that refer to registration under the ACNC Act;

(e) the extent (if any) to

which the registered entity is conducting its affairs in a way that may cause

harm to, or jeopardise, the public trust and confidence in the not‑for‑profit

sector mentioned in subsection 15‑5(1) (Objects of the ACNC Act);

(f) the welfare of members

of the community (if any) that receive direct benefits from the registered

entity;

(g) any other matter that

the Commissioner considers relevant.

·

The

Australian regulator’s secrecy provisions prohibit the regulator from publicly explaining

in detail the reason for deregistration decisions. In contrast, the NZ regulator publishes most eligibility

decisions in detail and has also published compliance deregistration decisions

in detail or released comprehensive detail about compliance deregistration

decisions to the media.

·

The

Australian regulator publishes a list of charity

compliance decisions on one easy-to-find webpage, whereas NZ does not separately

identify compliance-related deregistrations (although they can be identified with

some effort using the advanced search function).

·

Once

a NZ charity has been deregistered the charity officer details remain on the

register, however in Australia the charity officer names and positions are

removed.

The

first two years of the ACNC’s operation had a significant focus on ensuring

charities on the register were still active, so many deregistrations were the

result of a register integrity exercise.

In its 2015

Annual Report the ACNC reported that 10 charities were deregistered as a

result of compliance investigations, 1,663 charities requested voluntary

revocation, and 5,500 were revoked because they were ‘double defaulters’ and

had not filed returns for two consecutive years. The regulator reported that since the

register was launched in 2012, over 9,000 charities have been removed or had

their status revoked.

At

the time of writing this paper, the ACNC has not published any financial

information datasets, so it is not possible to analyse the financial statements

lodged by deregistered charities.

Data references

Data for this paper was

extracted from the New Zealand charity register (at www.charities.govt.nz) on 8 November 2015.

Disclosure

I

worked for the New Zealand Charities Commission and the Australian Charities

and Not-for-profits Commission from 2011 to August 2015. The above analysis does not take into

account any protected information obtained during my time at the charity

regulators. Any errors and opinions are

mine and opinions do not represent the views of my previous employers.

Further reference

You are welcome to join my existing 90 CharitywatchAu&NZ twitter followers (I only tweet about charity news and information) at https://twitter.com/StuDonaldsonNZ

You are welcome to join my existing 90 CharitywatchAu&NZ twitter followers (I only tweet about charity news and information) at https://twitter.com/StuDonaldsonNZ

I first wrote about

deregistered charities in Blog

No. 9 - Deregistered Charities

back in November 2012, so read that blog for an historical snapshot of

deregistrations. Now there is more trend

data and a lot has changed, including the regulator’s approach to deregistering

after two years instead of one year.

Thanks for reading my blog. Don’t forget to click on the advertisements for my

blog coffee fund! Cheers J

12 comments:

$$$ GENUINE LOAN WITH 3% INTEREST RATE APPLY NOW $$$.

Do you need finance to start up your own business or expand your business, Do you need funds to pay off your debt? We give out loan to interested individuals and company's who are seeking loan with good faith. Are you seriously in need of an urgent loan contact us.

Email: shadiraaliuloancompany1@gmail.com

LOAN APPLICATION DETAILS.

First Name:

Last Name:

Date Of Birth:

Address:

Sex:

Phone No:

City:

Zip Code:

State:

Country:

Nationality:

Occupation:

Monthly Income:

Loan Amount:

Loan Duration:

Purpose of the loan:

Email: shadiraaliuloancompany1@gmail.com

$$$ GENUINE LOAN WITH 3% INTEREST RATE APPLY NOW $$$.

Do you need finance to start up your own business or expand your business, Do you need funds to pay off your debt? We give out loan to interested individuals and company's who are seeking loan with good faith. Are you seriously in need of an urgent loan contact us.

Email: shadiraaliuloancompany1@gmail.com

LOAN APPLICATION DETAILS.

First Name:

Last Name:

Date Of Birth:

Address:

Sex:

Phone No:

City:

Zip Code:

State:

Country:

Nationality:

Occupation:

Monthly Income:

Loan Amount:

Loan Duration:

Purpose of the loan:

Email: shadiraaliuloancompany1@gmail.com

Greetings,

I am James Parker a loan lender from Unity Firm Financial Help, We give credit for business development, investment goals and for any purpose. Our credit is very affordable, fast and low interest of 3%. If you need a loan please do not hesitate to contact us via

Name: James Parker

Email: unityfirmfinancialhelp@gmail.com

Good Day Sir/Madam: Do you need an urgent loan to finance your business or in any purpose? We are certified and legitimate and international licensed loan lender we offer loans to Business firms. Individuals, companies firms, corporate bodies at an affordable interest rate of 3%. It might be a short or long term loan or even if you have poor credit. We shall process your loan as soon as we receive your application. We are an independent financial institution. We have built up an excellent reputation over the years in providing various types of loans to thousands of our customers. We offer Educational loan, Business loan, home loan, Agricultural loan, Personal loan, Auto loan with either a good or bad credit history. If you are interested in our above loan offer you are advice to fill the below information and return to us for more details. You can contact us with this email (standardonlineinvestment@gmail.com) we shall respond to you as soon as we receive your loan application details below.

First name:

Middle name:

Date of birth (yyyy-mm-dd):

Gender:

Marital status:

Total Amount Needed:

Time Duration:

Address:

Currency Needed

City:

State/province:

Zip/postal code:

Country:

Phone:

Mobile/cellular:

Monthly Income:

Occupation:

Which sites did you know about us.....

( standardonlineinvestment@gmail.com )for immediate attention. Contact

us now and get an urgent loan within two (2) days!!!

Regards,

Mr Abdul Muqse

Do you need Personal Loan?

Business Cash Loan?

Unsecured Loan

Fast and Simple Loan?

Quick Application Process?

Approvals within 24-72 Hours?

No Hidden Fees Loan?

Funding in less than 1 Week?

Get unsecured working capital?

Email us:urgentloan22@gmail.com

Application Form:

=================

Full Name:................

Loan Amount Needed:.

Purpose of loan:.......

Loan Duration:..

Gender:.............

Marital status:....

Location:..........

Home Address:..

City:............

Country:......

Phone:..........

Mobile / Cell:....

Occupation:......

Monthly Income:....

Email us (urgentloan22@gmail.com)

Are you a business man or woman? Do you need funds to start up your own business? Do you need loan to settle your debt or pay off your bills or start a nice business? Do you need funds to finance your project? We Offers guaranteed loan services of any amount and to any part of the world for (Individuals, Companies, Realtor and Corporate Bodies) at our superb interest rate of 3%. For application and more information send replies to the following E-mail address: standardonlineinvestment@gmail.com

Thanks and look forward to your prompt reply.

Regards,

Abdul

Hello Everybody,

My name is Mrs Sharon Sim. I live in Singapore and i am a happy woman today? and i told my self that any lender that rescue my family from our poor situation, i will refer any person that is looking for loan to him, he gave me happiness to me and my family, i was in need of a loan of $250,000.00 to start my life all over as i am a single mother with 3 kids I met this honest and GOD fearing man loan lender that help me with a loan of $250,000.00 SG. Dollar, he is a GOD fearing man, if you are in need of loan and you will pay back the loan please contact him tell him that is Mrs Sharon, that refer you to him. contact Dr Purva Pius,via email:(urgentloan22@gmail.com) Thank you.

Are you a business man or woman? Do you need funds to start up your own business? Do you need loan to settle your debt or pay off your bills or start a nice business? Do you need funds to finance your project? We Offers guaranteed loan services of any amount and to any part of the world for (Individuals, Companies, Realtor and Corporate Bodies) at our superb interest rate of 3%. For application and more information send replies to the following E-mail address: standardonlineinvestment@gmail.com

Thanks and look forward to your prompt reply.

Regards,

Abdul

Private Lender Bentex Funding Group Ltd.

Greetings to you by (BFGL).

We are a France-Paris based investment company known as Bentex Funding

Group Ltd working on expanding its portfolio globally and financing

projects.

We would be happy to fund and invest with you in any profitable

project if you have any viable project we can finance by making mutual

investment with you. If you are interested, kindly contact us

on:avitinvestmentauthority2@gmail.com for more details.

Looking forward hearing from you soonest.

Yours truly,

Mrs Rose Larsson.

(Personal Assistant)

Bentex Funding Group Ltd(BFGL)

509 Rue Jacques Coeur,75008 Paris-France

Paris-France.Bentex Funding Group Ltd (BFGL)

Are you a business man or woman? Do you need funds to start up your own business? Do you need loan to settle your debt or pay off your bills or start a nice business? Do you need funds to finance your project? We Offers guaranteed loan services of any amount and to any part of the world for (Individuals, Companies, Realtor and Corporate Bodies) at our superb interest rate of 3%. For application and more information send replies to the following E-mail address: standardonlineinvestment@gmail.com

Thanks and look forward to your prompt reply.

Regards,

Muqse

What are your Financial needs? We give out loans from a minimum of $5,000 to a maximum of $500,000,000.00 with comfortable duration that ranges from 1 to 30 years at a very reduced interest rate of 3%. Contact us via email: standardonlineinvestment@gmail.com

Thanks and look forward to your prompt reply.

Regards,

Muqse

PLEASE READ!!!! PLEASE READ!!!! PLEASE READ!!!! PLEASE READ!!!!

Hey Guys!!!Am so happy I got mine from Mike Fisher. My blank ATM card can withdraw € 2,000 daily. I got it from Her last week and now I have €14,000 for free. The blank ATM withdraws money from any ATM machines and there is no name on it, it is not traceable and now i have money for business and enough money for me and my family to live on . I am really happy i met Mike Fisher because i met two people before her and they took my money not knowing that they were scams. But am happy now. Mike Fisher sent the card through DHL and i got it in two days. Get your own card from her now she is not like other scammer pretending to have the ATM card, She is giving it out for free to help people even if it is illegal but it helps a lot and no one ever gets caught. i'm grateful to Mike Fisher because she changed my story all of a sudden . The card works in all countries except, Mali and Nigeria. Mike Fisher email address is : blankatm002@gmail.com

Get your business projects funded on debt basis and qualify for further cooperation on partnership basis after the repayment period. The funds can be accessed by startup and expanding companies.

Contact me for more information.

Email: standardonlineinvestment@gmail.com

Post a Comment